Data on federally inspected slaughter (AMS report SJ_LS 711) indicate significantly more cows are being slaughtered as percent of the total for the week, suggesting overall dressed weights will remain relatively low.

For the week ending Oct. 28, the AMS report indicates steer and heifer carcass weights have climbed to their highest levels since early January. However, these weights remain 16 and 11 pounds, respectively, below levels for the same period the previous year.

Beef production in 2018 is projected higher by about 325 million pounds from the previous month to 27.6 billion pounds. The 4.6 percent increase in beef production from 2017 is based on continued large feedlot placements in second-half 2017 and first-half 2018, leading to higher marketings and fed cattle slaughter in 2018.

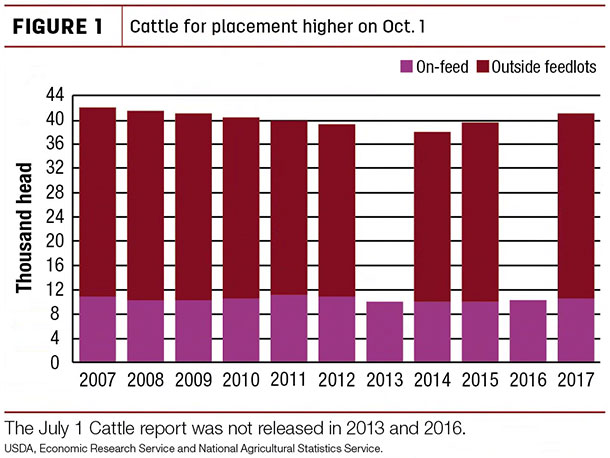

Comparing 2017 to 2015, the figure indicates there were 5.7 percent more cattle on feed and 2.9 percent more cattle outside feedlots waiting to be placed on Oct. 1.

Comparing 2017 to 2015, the figure indicates there were 5.7 percent more cattle on feed and 2.9 percent more cattle outside feedlots waiting to be placed on Oct. 1.

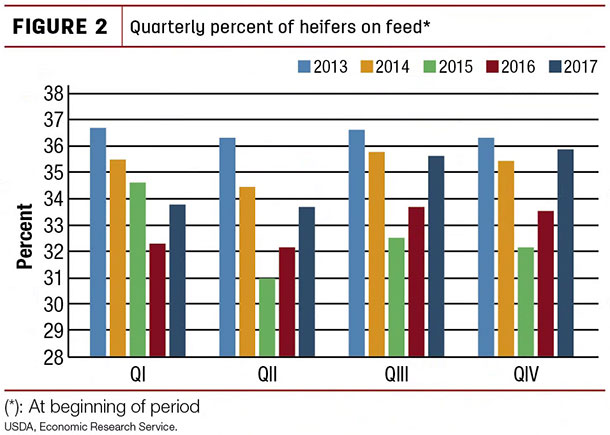

An increase in overwinter forage availability and a larger calf crop likely support the strong placements in 2018. The increase in the proportion of heifers on feed on Oct. 1, 2017, may reflect that a modest retention of heifers for breeding supports more heifers to be placed on feed in the coming months.

Based on strong margins at the retail and packer level, demand is expected to encourage feedlots to market cattle at a timely pace in 2018.

Strong demand to drive cattle prices up through early 2018

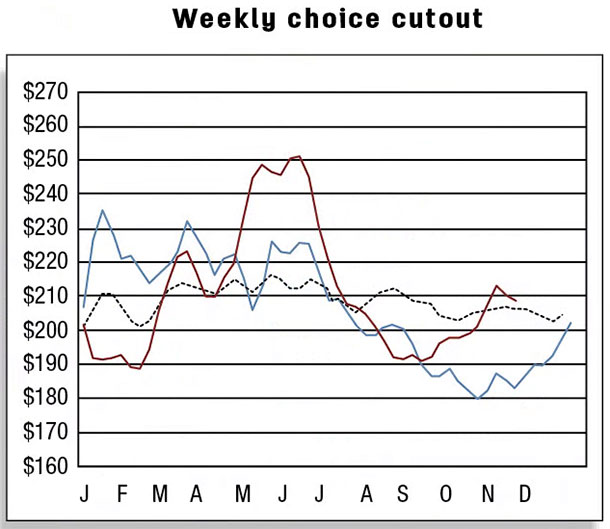

For most of 2017, market demand has pulled cattle through U.S. feedlots at a rapid pace, which has likely kept dressed weights lower than the previous year and limited the number of cattle in feedlots over 150 days. At present, packers may be forced to bid up prices because feedlots do not have an incentive to sell below their breakeven prices, in light of low feed costs and high futures prices for December and February.

With strong demand for beef and continued firm packer margins, fed cattle prices for the fourth quarter are expected to average above the previous year. However, in the first half of 2018, fed prices are expected to be below those of 2017, reflecting increasing supplies of slaughter-ready cattle.

The fourth-quarter forecast for fed steer prices was raised from the previous month to $117 to $121 per hundredweight (cwt), and the forecast for the first quarter of 2018 was raised to $116 to $124 per cwt.

The price forecast for medium-frame No. 1 feeder steers 750 to 800 pounds was raised to $155 to $159 per cwt for the fourth quarter of 2017. The forecast for 2018 feeder steers was also raised to $144 to $152 per cwt in the first quarter and $143 to $153 per cwt in the second quarter.

U.S. beef imports raised for 2017

Beef imports were up 5 percent in September from a year earlier to 231 million pounds. Among the major sources of imported beef, increased imports from Australia (+20.2 million pounds) and Mexico (+4.2 million pounds) more than offset declines from Brazil (-10.4 million pounds) and Uruguay (-2.3 million pounds).

As a result, imports during third-quarter 2017 were 8.4 percent (+63 million pounds) higher than third-quarter 2016. The forecast for fourth-quarter 2017 imports was raised by 10 million pounds from the previous month based on sustained demand for lean meat in the U.S. and increased imports from Mexico. The forecast for 2018 beef imports was unchanged from the previous month.

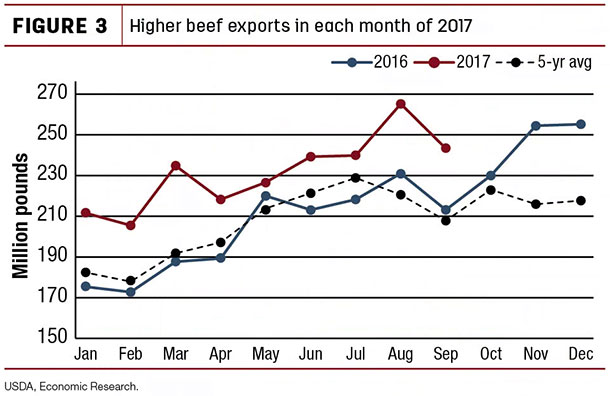

U.S. beef export demand strength continues

In September, U.S. beef exports reached 243 million pounds, a 14 percent jump year-over-year, largely due to elevated shipments to Japan (+20.9 million pounds). As a result, third-quarter 2017 exports were up 13 percent (+85.4 million pounds) from the previous year to 746 million pounds.

Based on the current pace of export growth, seasonal fourth-quarter export patterns and stronger weekly export sales data (USDA Foreign Agricultural Service) in October, the U.S. beef export forecast for fourth-quarter 2017 was raised by 30 million pounds from the previous month.

Higher domestic production, lower prices and stronger demand in overseas markets are likely to continue the competitiveness of U.S. beef for the rest of 2017 and through 2018. The forecast for 2018 beef exports was raised slightly to 2.9 billion pounds.

Cattle imports lowered and exports raised for 2017 and 2018

The U.S. cattle import forecast for 2017 was revised downward by 10,000 head from the previous month. A slower pace of U.S. cattle imports during August and a decline in imports in September resulted in a 3 percent growth in imports from January through September 2017 relative to the previous year to 1.275 million head.

September 2017 cattle imports were 6,708 head lower than the same month the previous year to 100,884 head. Imports declined from Canada (-9,510 head), outweighing increases from Mexico (+2,802 head). The cattle import forecast for 2018 was also lowered by 10,000 head from the previous month.

September 2017 cattle imports were 6,708 head lower than the same month the previous year to 100,884 head. Imports declined from Canada (-9,510 head), outweighing increases from Mexico (+2,802 head). The cattle import forecast for 2018 was also lowered by 10,000 head from the previous month.

Cattle exports for 2017 were raised by 15,000 head from last month’s forecast, based on higher year-to-date growth and expected seasonally higher fourth-quarter exports.

Exports through September of 97,986 head are more than double last year’s exports during the same period. U.S. cattle shipments through September are higher to both Canada (+44,942 head) and Mexico (+7,939 head) compared to the previous year. The forecast for 2018 cattle exports was also adjusted higher by 15,000 head. ![]()

Analyst Lekhnath Chalise assisted with this report.

References omitted but available upon request. Click here to email an editor.

Russell Knight is a market analyst with the USDA – ERS. Email Russell Knight.