Combined with severe alfalfa winterkill in parts of the Midwest, terms like “scarce” and “disaster” were being used to describe forage conditions and compelling leaders of agricultural organizations to seek flexibility in USDA crop programs to address current and impending forage shortages. All those forces helped push U.S. average hay prices to their highest level in five years.

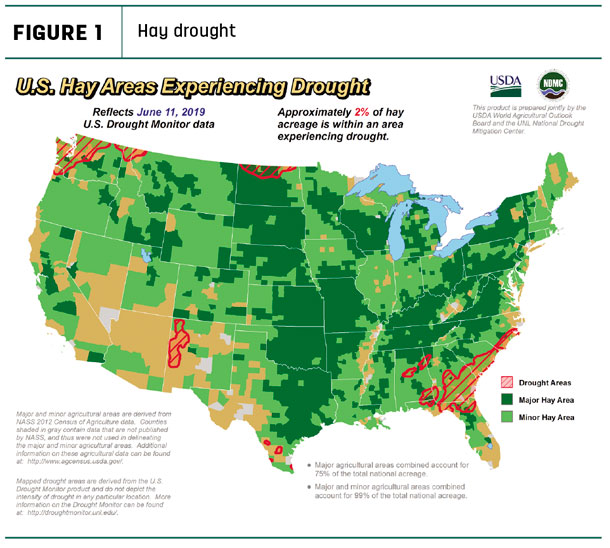

Drought areas few, far between

The USDA’s Weekly Weather and Crop Bulletin, updated June 11, indicated farmers in the Plains and Midwest were finally gaining traction in the fields, although wet fields and flooded lowlands remained.

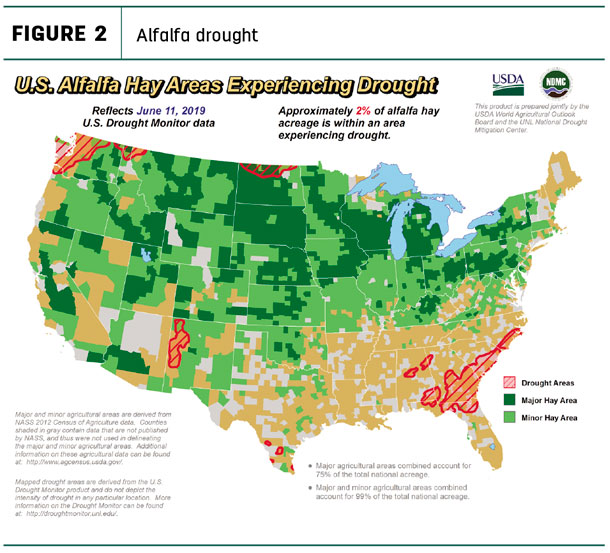

With large swaths of the country trying to dry out, areas highlighted on the USDA’s weekly drought monitor continued to be the smallest in a decade. About 2% of U.S. hay-producing acreage (Figure 1) and alfalfa-hay producing acreage (Figure 2) was considered drought areas as of June 11. Dry pockets are emerging in some hay-growing areas of the Southeast, northwest New Mexico, North Dakota and Washington.

Hay prices rebound sharply

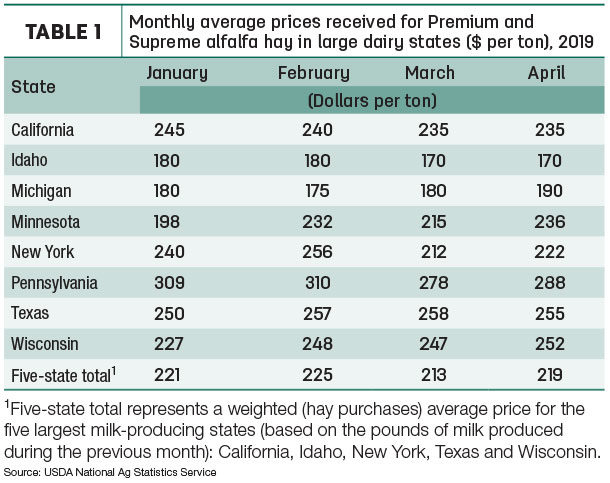

The need for dairy hay and a somewhat brighter outlook for milk prices helped Premium and Supreme alfalfa hay prices rebound in April. The USDA’s National Ag Statistics Service summarizes prices for “dairy-quality” hay in the top milk-producing states, averaging prices for the top five: California, Idaho, New York, Texas and Wisconsin (Table 1). April 2019 prices in those states averaged $219 per ton, up $6 from March.

Alfalfa

U.S. average prices for all alfalfa hay surged to $199 per ton in April, the highest since August 2014.

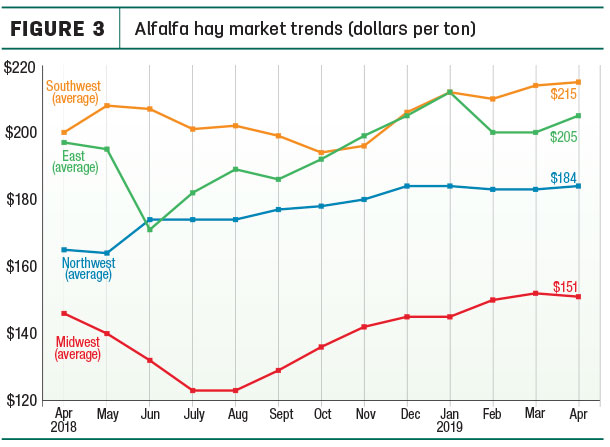

Compared to a month earlier, prices rose in the East, fueled mostly by a $20-per-ton increase in New York. Across other regions, price changes were mostly flat (Figure 3). Among individual states, Arizona, Michigan, Oklahoma, Oregon and Washington reported gains of $10 per ton, while Wisconsin led decliners, down $20 per ton.

Compared to a year earlier, alfalfa hay prices were up $56 per ton in Pennsylvania, $40 in Colorado, and $30-$35 in Minnesota, New Mexico and Utah. Ohio reported the biggest price drop, down $25 per ton from April 2018.

High monthly alfalfa hay prices were in New Mexico ($245), California and Colorado ($230), and Arizona and Kentucky ($220). The low price for the month, at $90 per ton, was in North Dakota.

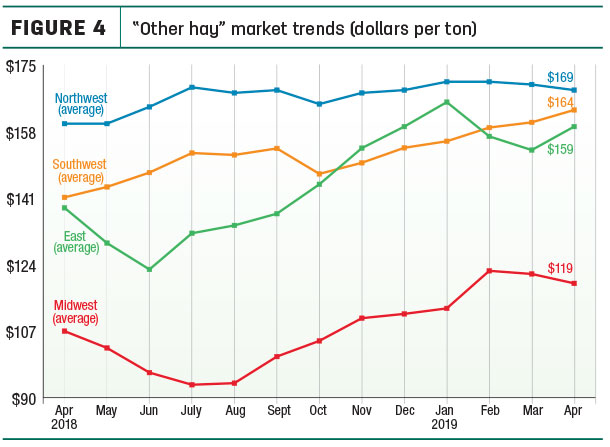

Other hay

The national average price for other hay was $151 per ton in April 2019, the highest since May 2014. Regional price increases were highest in the East and Southwest, with slight declines in the Midwest and Northwest (Figure 4).

Among individual states, Oklahoma and New York saw the largest month-to-month increases, up $23 and $20 per ton, respectively, while the average price was down $18 per ton in Minnesota. Compared to a year earlier, April 2019 prices were up $35 or more in seven states, led by New York (+$46) and California (+$45).

Highest average prices for other hay in April were in Colorado ($220 per ton), Arizona ($200) and Pennsylvania ($196). On the other end of the spectrum, the average price in North Dakota was just $71 per ton.

Organic hay prices

No sales prices for organic hay were reported in the USDA’s latest summary.

Hay exports on trend, in transition

U.S. hay exports maintained recent trends in April, as both buyers and sellers closed out one marketing year and began looking ahead to another. However, marketing relationships in search of steadying influences, comfort and confidence are being further complicated by trade wars, according to Christy Mastin, international sales manager with Eckenberg Farms Inc., Mattawa, Washington.

April and May are generally a time of declining hay inventories, and this spring saw supplies tighter than most years. With old-crop carryover supplies already low, a hard, extended winter increased domestic demand for supplemental hay feeding, eating into exportable inventories – and pushing prices higher.

At 111,680 metric tons (MT), April U.S. shipments of other hay declined about 13,000 MT from March; April sales were valued at $37.9 million.

Japan remained the most prolific buyer of other hay, topping 60,000 MT for the fourth consecutive month. Sales to three other major foreign markets – South Korea, Taiwan and United Arab Emirates (UAE) – were down slightly from March but were within a range established over recent months.

April alfalfa hay shipments totaled 215,592 MT – down slightly from March – and were valued at $68 million. Among leading markets for alfalfa hay, China returned to the top spot despite the ongoing trade and tariff war with the U.S. At 60,943 MT, it was China’s largest purchase on a volume basis since last September.

Japan wasn’t far behind, buying 56,944 MT. Sales to Saudi Arabia were the strongest since last November, but volumes to the UAE, South Korea and Taiwan were all down from March.

Moving into early June, foreign buyers were actively looking for alfalfa, but rain events during the first cutting hurt protein and relative feed values in the Pacific Northwest, pushing quality below what most foreign customers are interested in, Mastin said. That has increased focus on second cuttings, and hope for good, consistent harvest weather and less turbulence in trade relationships.

Regional markets

Back home, a summary of early June conditions and markets included:

• Midwest: In Indiana, Michigan and Ohio, harvest was delayed by wet field conditions.

In Minnesota, prices were steady with light demand and very little hay available.

In Wisconsin, cool and wet weather conditions delayed hay growth. Many farmers were running out of forage. Quality hay was in short supply and buyers are paying higher prices for lower-quality hay. Many farmers were scratching for forages because of extensive winter injury or lost alfalfa stands.

In Iowa, first cutting was about two weeks behind average. With very little 2018 hay left to be sold, livestock producers were growing desperate. What hay that was left was of low quality.

In Nebraska, alfalfa weevils and wet spots meant some farmers were cutting parts of fields in hopes they can put up some hay in great condition. There were reports of more alfalfa hay stored as balage and haylage across the state. New-crop alfalfa was going to dairies at $1.05 per point on relative feed value. Demand and prices were stronger for dehydrated and sun-cured alfalfa pellets.

In Kansas, hay market activity was slow, despite increasing inquiries from Eastern states. Prices remained mostly steady for old-crop hay, but new-crop pricing was all over the map. Producers were frantically swathing and baling hay before the next rain shower, with warnings to watch for flood debris. Most reported the first cutting was going directly to the grinder market. Very little dairy-quality hay had been baled, and a lot of early hay was wrapped due to the lack of good hay-curing weather.

In Missouri, early June harvest was well behind the five-year average. Due in part to the poor hay curing weather and shortage of inventory, there was a tremendous amount of early hay wrapped this year. Those conditions combined to support prices, but new-crop hay sales were limited.

In South Dakota, hay prices were higher with very few sales reported.

Growers had started to cut and bale new crop hay, bringing much-needed supply stability.

• Southwest: In California, hay harvest picked up the pace as rains subsided.

In Oklahoma, heavy rains, flooding and tornados left hay markets unestablished.

Rain hampered hay harvest and quality in much of Texas, but pastures were in good conditions, limiting the need for supplemental feeding.

In New Mexico, alfalfa hay in large bales sold steady on good demand.

The southern region continued their second cutting; the southeastern and eastern region were almost done with first cutting.

• Northwest: In Idaho, unseasonably cold, wet weather delayed first cutting, in some cases pushing hay maturities past ideal stages. Hay trading was inactive.

In Colorado, light seasonal trade activity has postponed regular market updates until mid-June.

In Montana, eastern growers were getting ready for first cutting. Moderate to heavy supplies of alfalfa hay in rounds sold generally steady in a light test; supplies of square bales were very light In Oregon, hay prices trended generally steady as storms in growing areas delayed harvest.

In the Washington-Oregon Columbia Basin, rain showers continued to affect hay that has been put down, resulting in lowered test results. Premium/Supreme non-rained-on new-crop alfalfa traded mostly steady.

In Wyoming, all forages sold steady on a thin test. Warmer weather was aiding growth, but most hay producers were looking at near the end of the month before new-crop alfalfa and grass hay would be ready to cut and bale.

• East: In Pennsylvania’s Lancaster area, market activity was light, limiting alfalfa price information.

In Alabama, hay prices were fully steady on moderate supplies and good demand.

Dairy outlook brightens a little

Declining cow numbers and slowing growth in milk output per cow doesn’t necessarily boost hay sales, but it may help improve the financial status of struggling dairy farmers. The USDA’s June World Ag Supply and Demand Estimates (WASDE) report cut milk production forecasts for both 2019 and 2020, providing at least minor support for milk prices. While still not out of the woods, projected prices for 2019-20 would be the highest in consecutive years since 2013-14. Dairy cull cow slaughter continues to outpace year-ago levels; as of mid-May, cow slaughter was running 60,000 head more than during the same period in 2018.

Beef outlook hinges on corn

May 1 cattle feedlot inventories were up 2% compared to a year earlier, the highest inventory for that date since the USDA began tracking inventories in 1996. However, with planting delays threatening to push corn prices higher, there may be more incentives to add weight to cattle on pasture, slowing the pace of feedlot placements going forward.

Figures and charts

Progressive Forage tracks regional hay price trends using average monthly prices reported for selected states by the USDA’s National Agricultural Statistics Service (NASS). The USDA report does not provide hay quality classes in its price reports. By region, states included:

- Southwest – Arizona, California, Nevada, New Mexico, Oklahoma, Texas

- East – Kentucky, New York, Ohio, Pennsylvania

- Northwest – Colorado, Idaho, Montana, Oregon, Utah, Washington, Wyoming

- Midwest – Illinois, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Wisconsin

-

Dave Natzke

- Editor

- Progressive Forage

- Email Dave Natzke