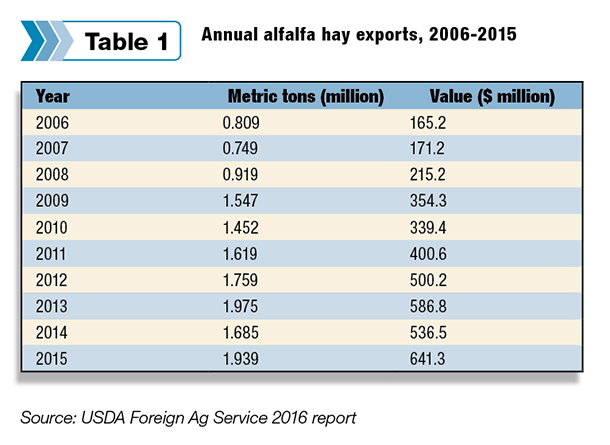

USDA released December 2015 and annual export totals on Feb. 5. For the year, U.S. alfalfa hay exports were estimated at 1.939 million metric tons, up about 15 percent from 2014, and just under the record total of 1.975 million metric tons exported in 2013.

Alfalfa hay exports were valued at about $641.3 million in 2015, up 20 percent from 2014, and the highest total on record.

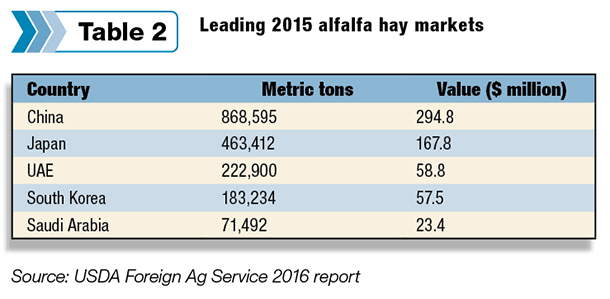

China was the leading U.S. alfalfa hay market in 2015, purchasing 868,595 metric tons, or about 45 percent of the total. Other leading markets were Japan, the United Arab Emirates (UAE) and South Korea.

Other hay

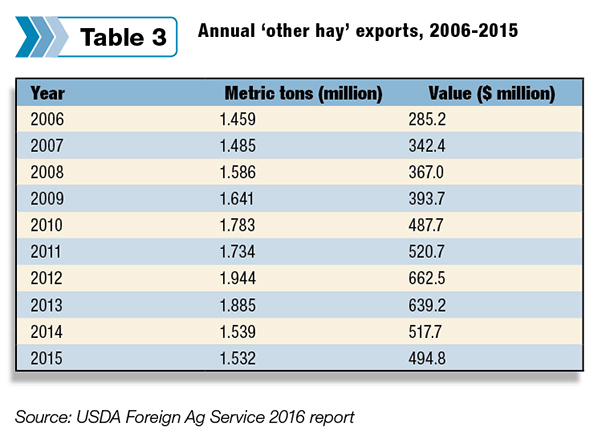

Meanwhile, 2015 U.S. exports of other hay were estimated at 1.532 million metric tons, down slightly from the year before, and the lowest annual total since 2007. The value of other hay exported in 2015 was estimated at $494.8 million, the lowest since 2010.

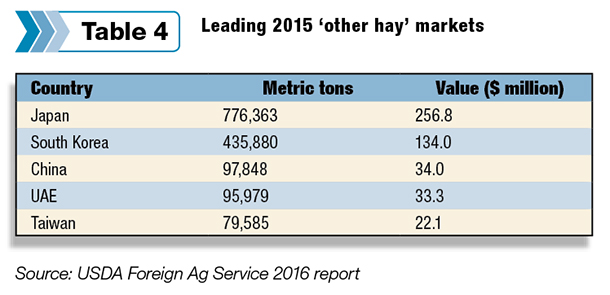

Japan remained the leading U.S. foreign market for other hay in 2015, at 776,363 metric tons, or about 51 percent of the total. Other leading markets were South Korea, China and the UAE.

Japan remained the leading U.S. foreign market for other hay in 2015, at 776,363 metric tons, or about 51 percent of the total. Other leading markets were South Korea, China and the UAE.

Export market challenges: Still feeling 2014

West Coast hay exporters faced significant challenges in 2014, influencing market dynamics throughout 2015. Those challenges are expected to continue impacting the industry in 2016, according to Northwest Farm Credit Services' latest hay market snapshot.

Export demand in 2014 was down due to high hay prices and the strong U.S. dollar. Exporters also experienced market disruptions, including worker slowdowns at West Coast ports and China’s adoption of more sensitive testing for genetically modified organisms (GMO) in hay, which resulted in a backlog of shipments.

Although port issues were resolved in early 2015 delivery of the delayed shipments resulted in a build-up in inventory for export customers. While these inventories have largely been worked through, exporters face the challenge of regaining lost business.

Foreign hay customers are sensitive to the reliability of hay supplies, sourcing feed from countries such as Australia, Spain and South Africa during the port slowdowns. These new relationships continue to the detriment of demand for U.S. hay.

Foreign hay customers are sensitive to the reliability of hay supplies, sourcing feed from countries such as Australia, Spain and South Africa during the port slowdowns. These new relationships continue to the detriment of demand for U.S. hay.

The value of the U.S. dollar increased significantly throughout 2015 as countries such as Japan and China devalued their respective currencies.

Dollar strength is expected to continue as the Federal Reserve gradually increases benchmark interest rates, and the global economy remains generally weak. Foreign competitors including Australia are benefiting from currency exchange advantages over the U.S. Australia has an added freight advantage that keeps costs lower.

Japan remains the largest and most mature hay export market. However, exports to Japan have been impacted by a declining and aging population and currency devaluation, according to Northwest FCS. South Korea is another mature market and is further challenged by a government quota system.

Japan remains the largest and most mature hay export market. However, exports to Japan have been impacted by a declining and aging population and currency devaluation, according to Northwest FCS. South Korea is another mature market and is further challenged by a government quota system.

Growth in hay exports to China is expected to continue for the foreseeable future. China relies on imported feed to support its growing commercial dairy industry. When considering “other markets,” volume increases were led by Saudi Arabia and Canada. Saudi Arabia is considered a burgeoning market for U.S. hay.

Similar to the UAE, Saudi Arabia is prioritizing water for food crops over feed crops. Smaller emerging markets in Vietnam, India, Malaysia and Indonesia are also expected to benefit the export industry long-term. The uptick in demand from Canada is likely a short-term phenomenon born of the same drought conditions that plagued the western U.S.

Similar to the UAE, Saudi Arabia is prioritizing water for food crops over feed crops. Smaller emerging markets in Vietnam, India, Malaysia and Indonesia are also expected to benefit the export industry long-term. The uptick in demand from Canada is likely a short-term phenomenon born of the same drought conditions that plagued the western U.S.

Increasing exports to China and Saudi Arabia generally favor exporters based out of California due to freight rate advantages out of the ports of Los Angeles and Long Beach. Northwest-based hay export companies continue to expand operations into southern California to take advantage of cheaper freight. FG