As in all industries, the dairy industry has become accustomed to continuous technological advancement. From stanchion to parlor to robot or from hay mow to silo to piles, we have seen the progression of technology over the years. It feels, however, that we have come to a point where our options for technology are endless. We can monitor seemingly endless metrics of our cows and barns, automate many redundant tasks on our operations, and utilize computer vision and machine learning to refine our management.

When we get into the weeds of all this technology, it becomes very difficult to decide which technology is right for our business. Even more, it is difficult to decide when to implement it. It requires a specific strategy to determine what, how much and when to invest in technology.

To start, a strategy is simply the plan you create to achieve your business goals. For most of us, the goal is to maximize profitability. It is important when approaching the conversation around technology that the basic goal of its implementation should be productivity – producing more with less. Don’t let the shine and intrigue of something new distract from the need to have it improve your bottom line.

To ensure the technology we are pursuing achieves the requirement of improving our bottom line, it is best to start from the bottom up instead of the top down. By this, I mean to start with a problem or bottleneck in your operation and seek out a solution, instead of starting with technology and hoping it provides extra value.

For a top-down example, parlor systems to collect individual daily milk weights are common technologies used by many dairies. I see the data collected is often incomplete and poorly utilized. For many, this is because the milk weights system was just an “add-on” when the parlor was built, and there wasn’t a clear plan on how to utilize the data. Thus, the data becomes inaccurate and unusable.

Now, let’s look at milk weights from the bottom-up perspective. If a dairy is looking to lower their expense of monthly milk testing or is looking to refine their culling strategies, they may look at a way to collect more routine milk data on-farm. Thus, they explore various meter systems for their parlor and find the correct one that fits their needs.

It may seem like a small nuance, the difference between bottom-up and top-down technology integration, yet I see hundreds of thousands of dollars wasted because there was never a clear business decision for the investment.

Once the business problem is identified, and we have decided to pursue technology to solve it, it is time to break out the pen and paper. When implementing any new technology, often the company selling it will provide some sort of return on investment (ROI). If they do not, ask for one. But also make sure to walk through one yourself. Actually write it down.

As an example, let’s assume we are exploring a rumination/activity monitoring system. We chose to pursue these because we felt our fresh cow check was taking too long and wanted to improve reproductive efficiency. The company said we would reduce on-farm death loss, lower cull rate and reduce days open. OK, now put numbers to it. It’s OK that we will have to make some assumptions. If we culled 20 more animals a year instead of dying on-farm, reduced milk lost from 50 animals because we caught them faster and lowered labor in the fresh cow pen by one hour a day, the system saved X dollars per year. Now we have something to approximate the return.

The final component of investing in technology is to determine when to pull the trigger. As we are all aware, technology only gets better. As soon as we buy our newest iPhone, Apple will already launch the next generation. So how do we know when is the right time?

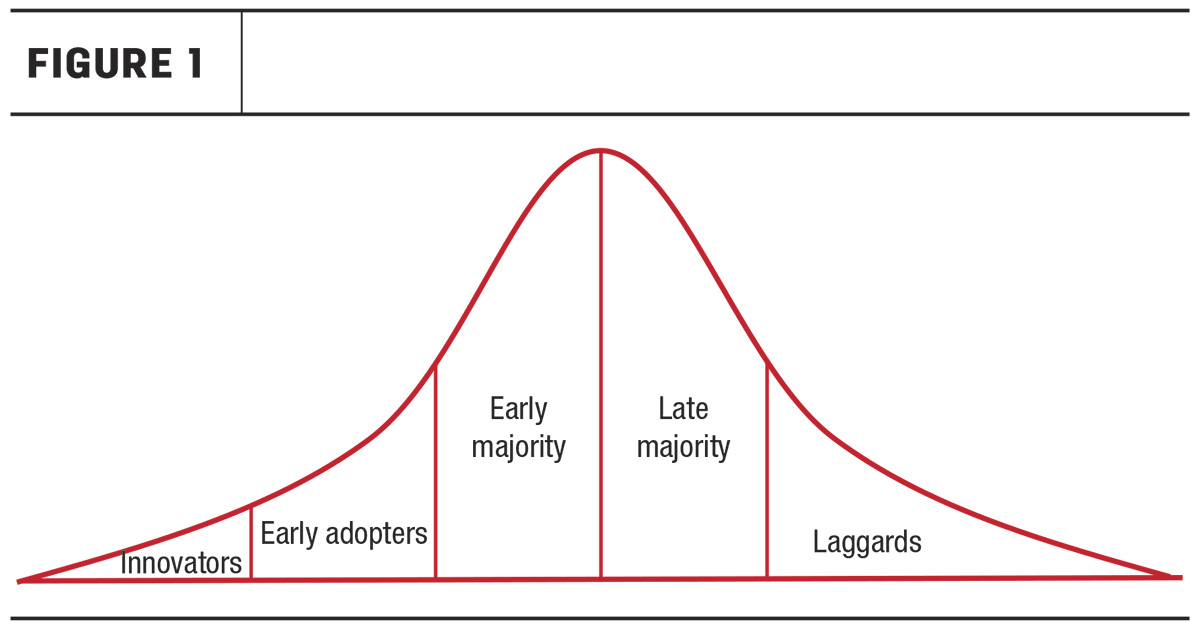

The “Technology Adoption Curve” (Figure 1) provides a good basis for how technology is generally accepted by a group over time. Even in the dairy industry, this curve transpires.

This curve breaks people into five groups based on the timing in which

they will adopt technology. Innovators are the fastest and are generally

asking for a technology before it was invented. Laggards are the

opposite and need a lot of time and encouragement to dip their toes into

the new technology. You may identify yourself or your competitors in

one of these groups.

As it pertains to the dairy industry, I do believe the “early majority” is the sweet spot to invest in technology. Waiting to be an early majority adopter allows a business to see the technology in action on other dairies, for the technology company to work out all the glitches and build a good support team and for the industry to better understand the ROI of the technology. Moreover, waiting for the early majority likely will not serve as a large competitive disadvantage to your business. Most technology provides only marginal improvements to a bottom line. There are not many technologies that will double a dairy’s profit.

The next time a new technology comes up in the management or team meeting, work through the process of identifying the business problem (bottom-up), determine the ROI and plan the timing of your investment. This short process can help refine your technology budget and ensure your business receives the most bang for the tech buck.